Helpful Steps to Recover from a Bankruptcy

Bankruptcy can feel like a death sentence. The shame alone is enough to make many people socially anxious. However, you can recover from a bankruptcy, and YES, there is life after bankruptcy. You can take steps back to financial health if you know what to do. It may not happen overnight but it will happen. You have to remain consistent and get to the heart of the problem so that you can grow your financial stability again. It’s been said many times and it must be said again, the journey of a thousand miles begins with one step. Financial health can be restored. You just have to be willing to be proactive. However, a proactive approach requires many different actions.

Steps to Recover from a Bankruptcy

There are many moving parts when it comes to patching up your financial situation. The first step is education and awareness. You must first understand your finances in terms of how much money you have coming in as well as how much money you have going out. It is also at stake to understand what areas you can change and adjust and which areas are engraved in stone or unchangeable. You must start with black and white facts which are made up of dollars and cents. This is the initial step. The next step is education followed by action. Rest assured, you can Recover from a Bankruptcy.

Money Matters

You need to become an expert in your financial situation. You may ask what this means. However, this is a simple question that’s easily answered. You need to know how much money you have coming in and how much you have going out. IN other words, how much do you make and how frequently? What bills do you have regularly? These are both important questions. If you can answer these questions you can take steps towards turning your financial situation around. However, everything must first come from the standpoint of creating clarity and awareness about your financial situation.

Create a Budget

You really can’t get too far without a budget. A budget creates boundaries that protect your financial health. Without one, it’s like walking around with a hole in your pocket. You don’t know how much to spend because you’ve set no clear rules for yourself and your vision is blurry. This is why the first step is the budget. Think of your budget as a roadmap. It will keep you on course and let you know when you’re veering off course as well. Plus, it must be a huge part of your solution if you want to Recover from a Bankruptcy.

Yes, You Do Need a Budget

When you sit down to create a budget, you must look at your financial situation in black and white. This means you need to know how much money you have coming in. You need a number or an approximation. After you’ve settled on that number, you need to write down all of your fixed expenses. In other words, expenses that don’t change but are due every month and typically the same amount. Once you’ve gathered all of your data, sit down and create a list with your revenue/ income and your fixed expenditures and variable expenditures. Start subtracting. Whatever is left after you’ve done all your math should go to your savings account. You should try to save at least ten percent of your income monthly.

Keep in mind that you may not be able to change your income but you can change your variable expenses by adjusting how much you spend. This is simple addition and subtraction. Don’t forget that your fixed expenses will be those recurring expenses like utility bills, your mortgage or rent, and your cable bill. However, variable expenses will be your grocery budget, the amount you spend on entertainment and personal care, and other expenses that you can adjust to suit your budget. You will have the greatest amount of wiggle room with your variable expenses. However, this is part of the critical thinking that will be required to Recover from a Bankruptcy.

I Have a Bankruptcy…What Next…

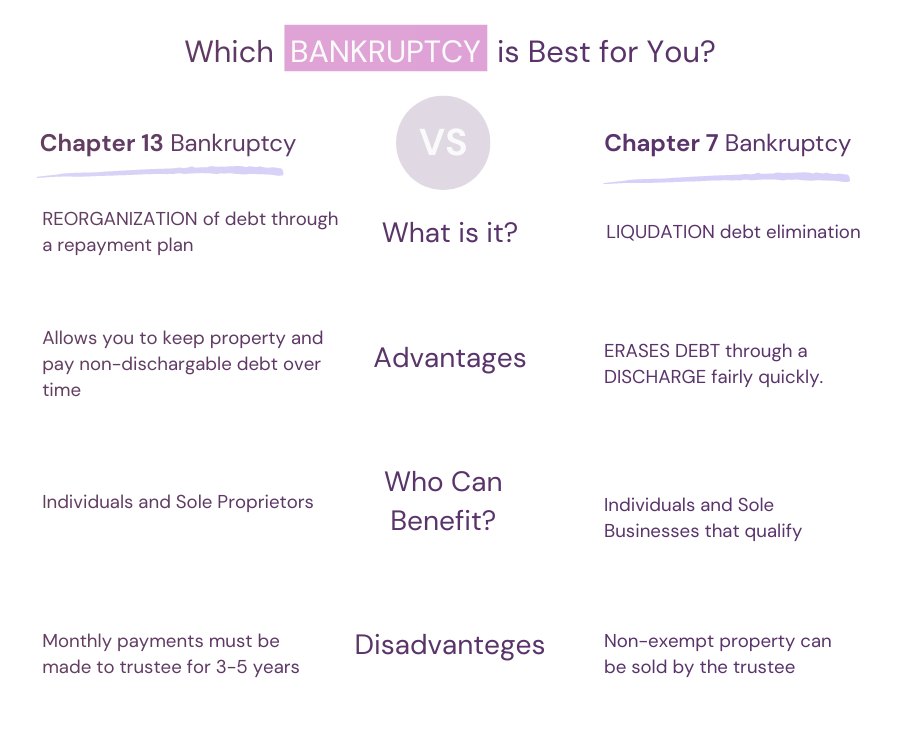

Many people may think that bankruptcy is an easy escape from the heavy load of debt, however, this is far from the truth. There are two common forms of bankruptcy that many people look into.

Chapter 7 was quite popular years ago

It absolved people of their debt by taking a person’s assets to help pay off their debts. However, this form of bankruptcy was/is harsh because, although it wipes away debt, a person may lose their home and other assets as a way of paying off debt. Plus, Chapter 7 doesn’t eliminate student loans, alimony, child support, or tax debt.

Chapter 13 is more common but it also comes with some harsh consequences

However, Chapter 13 isn’t quite as stark as filing for Chapter 7 bankruptcy. Chapter 13 works similarly to debt settlement and debt counseling. The court assigns you a trustee who negotiates with your creditors to pay off your debts. You make payments to the trustee, who, in turn, pays your creditors. The court must accept these payment arrangements, however. You are unable to open up any more lines of credit once you file for Chapter 13.

Although Chapter 13 has become more popular than Chapter 7, it has more negative ramifications. However, regardless of the type of bankruptcy, you can still recover. A careful assessment of your situation and the options you have available to you can help guide your path. You can recover from a bankruptcy.

Should You Contact a Debt Counseling Company for Help?

If you feel weighed down by your debt you may feel that you need help when it comes to navigating this issue. You can Recover from a Bankruptcy. There are debt counseling companies that exist for this express purpose. A debt counseling company will take a look at your debts and give you advice on the best way of paying off debt and resuming your financial situation. Some companies will even take your money and pay these companies for you. These companies exist for the primary reason of educating you and providing specific advice on your situation.

This is the true value of debt counseling. You can walk away with expansive financial information that can help you with your current situation as well as your future financial goals. If nothing more, these companies save you the time and effort it would take to find this savvy information yourself. They provide key information at your fingertips. This is perhaps why these types of companies may make sense for people who don’t want to invest the time and effort into finding all this vital information themselves. Also, a debt counseling company will help you create or tweak your budget which will help you reach your financial goals as efficiently as possible.

This is free financial advice. Many of these financial wellness programs can enlighten the consumer and put them in a better position to have mastery over their finances. Also, many debt counseling companies may be able to lower your interest rates or set up a more manageable payment plan. However, they can make your debts more manageable and user-friendly.

What Is Debt Settlement and Should I Consider It?

Debt counseling can be a great resource when it comes to getting financial information and guidance on your specific situation. It does have value. However, some people consider debt settlement as a way of reducing their debt. This process involves working with a financial company to negotiate a lesser payment for the debts you owe. These companies will work directly with the companies you owe to reduce the amount you owe and set up payment arrangements that will be more manageable for you to handle. However, more often than not, if these companies can renegotiate and reduce your debt the reduced debt is usually due in a lump sum. The reduced debt is usually not broken into payments.

Shop for a Debt Settlement Company

There are many debt settlement companies out there. This is why you must do your homework. You need to have your ear to the ground to get the truth of how effective a company is. This is why it’s not a good idea to rely on the reviews you find on a debt settlement site. You need to look for unbiased opinions on the company. How much have they helped customers in the past? What exactly do they do? How long have they been in business? What kind of results can you expect, typically? These are all extremely important questions that should be answered thoroughly before you settle on a company. Also, you need to know how much the services will cost. You will also need to inform the company of any debts you may have that don’t appear on your credit report.

Once you have done your homework, you will need to make sure that you’re following the agreed-upon terms of your repayment or you renegotiated pay off. However, it should be noted that a debt settlement and an original debt don’t make much difference when it comes to your credit. As long as you pay the settlement amount of the original debt your credit will benefit and gain almost the same amount of points either way. A debt settlement company can be instrumental in helping you Recover from a Bankruptcy.

Debt Settlement or Debt Counseling?

You may ask what type of program would benefit you the most, however, the answer is intensely personal. You may need to seek debt counseling as a way of deciding which approach would be best for you. IN general, if the amount of debt you are facing is extremely large in comparison to the amount of money you have coming in, debt settlement may reduce some of that burden by diminishing the amount that you owe. In instances like this, seeking debt settlement may be able to provide some real relief. However, you may want to get some counseling regarding which direction to go. In short, you may benefit from utilizing both debt counseling and debt settlement.

However, some people may not need a debt counselor to tell them that they should consider debt settlement. These people know that they would benefit from any reduction to the amount of debt that they owe. These are the people that would benefit from debt settlement and don’t need a professional to tell them this. However, both companies can be beneficial to Recover from a Bankruptcy.

The Bottom Line…

There are tools and organizations that you can use to restore your financial health and recover from a bankruptcy. However, you must dig deep into your financial situation and get organized to make a dent when it comes to restoring your financial health.

Get Organized

The first step is to get organized. This is perhaps the most tedious step. You’re going to need to pull out all your financial documents and get everything organized. This may mean that you need to take a few hours on your day off to get everything together. However, this will help you to build a realistic roadmap of where you stand from a financial standpoint. Pull out your bills, receipts, and any other financial documents that will help you create a realistic picture of your financial obligations and debts. The rule to this is to leave no stone unturned. This is the only way you’re going to get a clear picture of where you stand.

Categorize Everything

Group the same types of bills and debts. For example, put all of your monthly bills in one stack, form another stack with your debt, receipts in another and so on. Make a list of your recurring bills along with their due dates. Add up those bills and make note of the total. Also, create categories for your normal household purchases as well as any and everything else that you spend money on. These areas should include your groceries, laundry detergent, cleaning supplies, and toilet paper. In essence, you need to account for every dime that you spend. This is where your receipts come in. Look through them with a fine-tooth comb and make a note of where your money is going.

The biggest part of getting your financial situation under control is awareness. You need to know where your money is going and how much you’re spending. It’s a good idea to use your receipts from the prior month to see where your money is going. Next, list your assets. This step represents things of value that you own that could be sold to help pay off debt. If you own big items that you could sell, like a car, be sure to use official data sources to determine their value. For example, the Kelley Blue Book or the NADA should be used to determine the value of your car. Itemize the value of everything on this list and make note of these values.

Create Two Main Categories

After you’ve organized your debts, separate them into two categories. The first category should include debts that must be paid in full. The second category should include debts that can be paid or settled for less than what you owe. Focus on the settlement debt first. Typically, settlement debt is usually older than the rest of your debt. These are bills that you’ve owned for a long time and the creditors are willing to negotiate and accept a lesser payment and consider the debt settled or paid in full.

Even if these settlement offers have expired, it is still likely that these companies would be willing to accept a settled amount of the debt. Simply call them and ask how much they would accept. It doesn’t take any special skills to do this. Creditors know how much they can accept on debt and will usually offer you this amount as a settlement.

Look At Your Money

The next step is to take a close look at your spending habits. How much money are you spending? How much of that money could be realistically redirected towards a debt? Readjust your spending to go towards a debt that can be settled for less. IN other words, take a good look at your variable expenses and determine where you could spend less to create more money to pay off a debt. Even if you don’t have all of the money, you can ask the creditor to give you thirty days to pay the settled debt amount in full.

This will require some sacrifice and the willingness to veer from your usual spending habits. Attacking your older bills that you have the option of settling will more than likely yield some results. Most creditors would rather get some money instead of none.

Launching a savings account can also be a good way to look at your money. You could probably start here!

Payment Plans

Some creditors won’t agree to give you thirty days to settle a debt, if this happens, ask for a payment plan and stick to it if they agree. In situations like this, a payday loan may be a solution if you can repay it quickly. Of course it should not be the first one! But we wanted to talk a bit about it just so that you know it exists. It may be worth it to take out a small loan to get an old bill out of the way and paid. Weigh your options and be smart. If you do opt to take out a payday loan, don’t let the fees accrue by letting the loan linger. As soon as you can pay off the payday loan, do so. However, do your homework. Be sure you can afford this type of loan and make sure to do your payday loan shopping before applying!

Also, if you have credit cards that will allow you to take a cash advance to cover the bill, consider this option. It’s easier than taking out a payday loan. You’re using the credit that you already have. All you have to do is pay the interest and fees back that the cash advance created. This is necessary to avoid inadvertently creating more debt than you need to.

Payday Loan Requirements

Most payday loans don’t have a lot of requirements and eligibility criteria can vary from company to company. However, a few of the requirements tend to be standard across the board. Most payday loan companies require that loan candidates be at least eighteen years old, have a checking account, and verifiable income. There may be other requirements but these are usually standard for most payday loan companies.

Payday Loans May Help…

Payday loans are usually high-interest unsecured loans that are designed to be paid back by your next payday. These types of loans have a few other names. They are often referred to as short term loans and cash loans as well as payday loans. They are designed to be paid off quickly because they typically have steep interest rates. In a bind, these loans could be used to pay off smaller debts if you could repay them fairly quickly. These loans are usually income-based instead of credit-based. However, they can be based on credit even though they usually aren’t. These loans are also typically five hundred dollars or less. If you know how to use these types of loans to your advantage, they can be quite helpful.

Can it be a smart move?

Taking out a payday loan can be a smart move to avoid finance charges on your credit card bill or late fees on your utility bills. But once again, it should not be your first solution as it is a risky way of escaping credit card late fees! They may save your credit by preventing you from accruing late payments. However, these loans aren’t designed to be kept over a long period because of the high-interest rates. You could end up paying back significantly more than you borrowed if you don’t pay these loans off quickly. They are known as convenience loans because they are usually fairly easy to acquire and many payday loans have an online presence which makes it easy to apply.

The funding tends to be fairly quick as well. Many online payday loan companies operate exclusively on the web, making it easy to apply, e-sign documents, and get funded in twenty-four to forty-eight hours. These loans can be used to help you crawl out of debt, which is beneficial to your financial health, by helping you to quickly pay off small bills. As long as you pay these loans back quickly, they can be a great resource when it comes to helping you recover from a bankruptcy.

Conventional Loans Might Help Too

Payday loans differ significantly from conventional loans in that they usually have easy qualifying terms, can be acquired quickly, and are designed to be paid off by the next payday. Conventional loans usually require good or at least fair credit and usually take time to get approved. However, conventional loans usually have a better interest rate and you can typically borrow more money with a conventional loan. If you have large debts that are accruing interest, you may benefit from a personal loan, particularly if the interest rate is lower.

If you have a significant bill that has a high-interest rate, taking out a personal loan may help you to eliminate that bill and pay less over time because the interest rate is lower. This is a substantial step in the right direction for your financial health and recover from a bankruptcy. A personal loan can be beneficial in helping you to recover from a bankruptcy.

How Do Personal Loans Work?

If you meet the requirements, personal loans can be a viable option when it comes to getting your financial situation together. This may be a helpful move to consider when you’re trying to climb out of the hole that bankruptcy has created for you. Personal loans typically have lower interest rates than payday loans and give you more time to pay them off. Plus, if they are handled well, they can help you to build your credit. This usually means that you are making your payments on time and following any other terms that may be included in your loan agreement.

Many people mistakenly believe that Chapter 7 bankruptcy prevents them from applying for a personal loan, however, it doesn’t. Of course, your chances of being approved for a personal loan may be significantly less, but it’s not impossible. Plus, as stated earlier, not only can a personal loan help you pay off debt, it can also help to rebuild your credit after a bankruptcy. It can do this by showing that you can make your payments on time and follow the terms of a loan. Both reflect positively on your credit. You have the option of applying for a secured or unsecured personal loan. A secured loan may be easier to acquire because the lender has less risk involved. A secured loan will generally be more difficult to acquire because there is a significant risk, particularly for those with a bankruptcy. However, it’s not impossible.

Can Credit Cards Help Rebuild Credit After Bankruptcy?

You can also use a credit card in similar ways. You can apply for a secured or unsecured credit card to rebuild your credit after a bankruptcy. Secured credit cards are much easier to qualify for because they are backed by your bank account or funds that you are required to pay upfront. However, unsecured cards aren’t impossible to get. They are just more difficult to acquire with bankruptcy and poor credit. However, both credit cards can help rebuild credit after bankruptcy by making your payments on time and following the terms of the credit card.

Closing Thoughts…

It may seem as if bankruptcy is a death sentence for your credit and your overall financial health, but it’s not. You can rise from the ashes even if you have a bankruptcy under your belt. However, it does require some financial savvy and education. You must be able to use all the tools in your arsenal to free yourself from your dent and regain your financial standing. This can be achieved through a wide variety of different measures. Also, it doesn’t necessarily require the use of debt counseling companies or debt settlement. You can do it on your own.

Of course, these companies can be beneficial in helping guide you back to financial health after a bankruptcy. However, each person’s situation is highly specific and what may work best for one person may not be the best for another. Financial health after bankruptcy requires gaining clarity and an in-depth understanding of your financial situation, how you get there, and the best way to regain your financial footing. But just keep in mind one thing: You can Recover from a Bankruptcy.

Nwayita Perry is a personal finance writer who knows the value of getting the most out of her dollars. She understands that financial savvy is the key to making her budget stretch. She takes pride in sharing her financial planning and spending advice generously and prolifically. Her passion lies in helping millennials, as well as people of all ages and from all walks of life, develop rich habits they can use for life.